2020: A Year Like No Other with a Mixed Outlook for Subsea

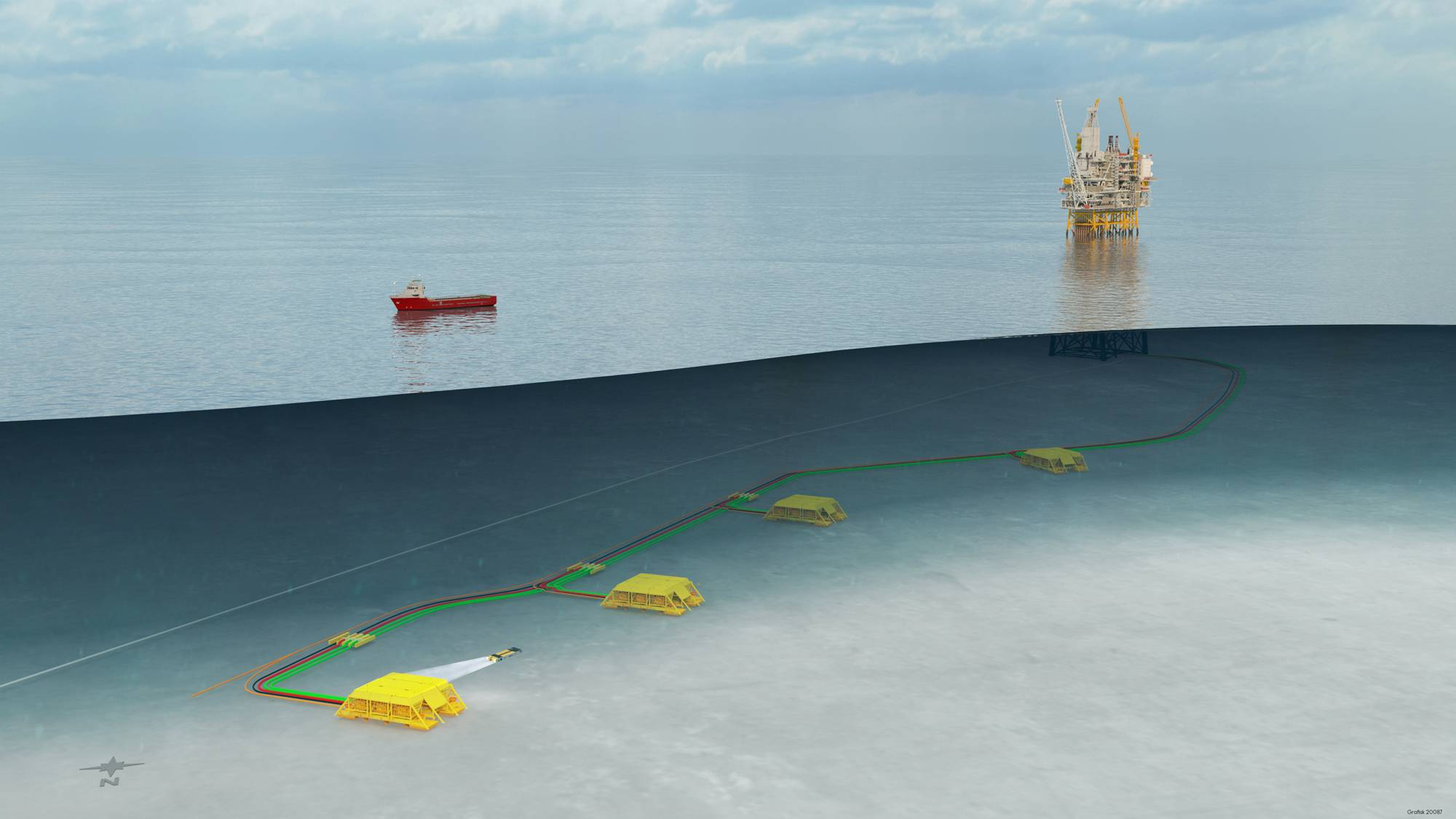

Equinor’s Breidablikk project in the Norwegian North Sea, with 23 wells, was one of four projects adding to subsea tree order numbers last year. Image copyright Equinor.

On many levels, 2020 was a pretty horrific year, “a year like no other”, according to Mike Beveridge, managing director of energy investment firm Simmons Energy, a division of Piper Sandler. It’s easy to see why. A dip into a negative WTI contract prices, Brent troughing at $23/b – the indicators were all pretty grim. The scary thing is, it could have been worse. But there is light at the end of the tunnel.

Speaking at the Society of Underwater Technology’s (SUT) annual subsea market outlook, usually held in Aberdeen, but this year held online, Henning Bjørvik, VP of energy research at Rystad, said that, with around 140 firm subsea tree awards in 2020, “We were basically now more or less back to what we saw in 2016,” a year which was a record low (around 100 trees).

The challenges, in 2020, multiplied. Coronavirus changed our lives, the energy transition gained pace and the threat of peak oil is now looming, Beveridge told the SUT event earlier this week (April 20).

While the intervention of OPEC+ improved prices (50% of global supply, while Russia remains in the group), it’s still a finely balanced market, he says. Anti-fossil fuel thinking has been gathering pace, the Biden administration has re-signed the Paris treaty, the UK government has committed to net zero and the country is hosting COP 26, while investors “continually shift their attention away from fossil fuels”, due to a realization that peak oil demand is on the horizon, Beveridge said, citing a recent report from Goldman Sachs which suggested anemic demand after 2025 and peak oil as early as 2026, a sentiment repeated by Rystad on Wednesday (April 21).

“Investors are increasingly focused now on carbon footprints, there’s more government policies, society’s demand, customers care what the emissions of their supply chain look like, employees care,” said Beveridge. Carbon taxes are coming, operators are looking to attract capital by being seen to be green and most oilfield services deals have to demonstrate to potential buyers how they’re service or technology helps to reduce emissions, he said. “This is a critical feature that didn’t exist in deal making two years ago.” It’s a tough environment for the oilfield services sector where equity values are 71% down compared to 2017, despite Brent having recovered 14%, he said.

For the subsea market, it’s been especially tough. Another slump down to around 140 firm subsea tree awards in 2020 was a major step down from the 530 per year ordered in the hey days of 2012-2013, and some way off the 300 or so that had been forecast for 2020, prior to the Covid pandemic and another drop in oil prices.

Prior to Covid, projects like Bay du Nord, Cambo and Rosebank were on the verge of being sanctioned. “But we’re not in this world anymore,” said Bjørvik. Last year, subsea tree ordered for Woodside’s Sangomar off Senegal, ExxonMobil’s Payara off Guyana, Equinor’s Breidablikk in the North Sea and Petrobras’ Mero III in Brazil’s Santos basin, made up the bulk of the subsea tree orders, Bjørvik said. “If those four projects weren’t moving ahead, 2020 would be a devasting year for the subsea market,” he told the SUT event.

But there’s hope within sight and “subsea players should be ready for a ramp up,” says Bjørvik. In Norway there has been a tax relief package, which has lowered breakeven prices by 40% on average and the results of that are being seen; there are a lot of projects in the pipeline, he says. Brazil is still ploughing ahead with its FPSO projects, Guyana will still also be there, as ExxonMobil forges ahead with its Stabroek block finds, which will require quite a lot of subsea trees.

“For subsea tree awards, we are a bit more bullish for 2021 compared with 2020,” says Bjørvik. That’s partly due to Petrobras’ Buzios tender, which includes 53 trees. Without Buzios, the forecast would be more like 2020. “So the real recovery, back to 2019 numbers (ca.300 trees), we see in 2022,” he says, “when there are a lot of competitive projects in the pipeline, and hopefully the covid situation has been resolved and the oil price is stable.”

More broadly, investment numbers are expected to ris, up to 2023, he says. Offshore greenfield project sanctioning is expected to increase from under US$50 billion in 2020 (just a bit above the 2016 low), to nearly $120 billion in 2023, says Bjørvik.

That raises a question; will the industry be able to meet the demand, he asks. While many have been able to live off their backlogs, order intake last year took a hit. “We are expecting to come back to 300 trees by 2022,” however, he says. But after dropping back to 140, can 300 be delivered and what will the impact be and should operators be concerned about capacity, asks Bjørvik.

He also says the future is likely to be dominated by scaled down and phased developments. “We see operators being focused on scaled down, phased and accelerated developments,” he says, which is likely to be positive for the subsea tieback market. At the same time, we’re likely to be moving towards the end of an era when it comes to mega-projects, he says. While there are a couple on the near-term horizon, such as Equinor’s Wisting and Bay du Nord projects, it’s otherwise hard to identify many mega-projects in the longer term, says Bjørvik.

For Beveridge, there’s some positivity in the North Sea, with newer operators in the basin, although there is a ‘but’. “I’m not negative about the North Sea, I think it’s reinventing itself again,” he says. “These new operators coming in are investing for the long term; they have clear strategies, access to capital and plans to develop their assets, as long as they have a license to operate and that that’s not taken away.”

While there are fewer private equity investors wanting to plough money in, there are still investment themes, around well decommissioning, brownfield and subsea IRM, robotics, AI, software and emissions analysis and reduction, he says.

Tellingly, an increasing focus at Simmons is in another sector; offshore wind. Floating offshore wind, specifically, is an incredibly exciting prize, says Beveridge. “The links between subsea oil and gas and floating wind are really quite pronounced,” he says. “You have massive know how sitting in our industry in areas like electric systems, cabling, mooring, floating infrastructure, repair and IRM of dynamic structures, that positions our industry incredibly well to capitalize on floating wind.” Time will tell, but the world does appear to be heading in one direction – the question is how quickly it will get there.